In this post, I want to analyse the current PASS situation, explain some broader context, and give people a more data-driven view. I hope that this leads to a calmer discussion by providing additional information and data. I want to help by providing data and insights on the recent PASS row online. I also want to sound a few warning bells and I have the data to back it up.

My analysis is based on the Financial statements put forward by PASS using some basic metrics; until you do that piece, you can’t move forward to compare and contrast it with other data since you have not done your ‘descriptive statistical analysis’ first to ensure that the comparison is valid. Basically, you have to note everything out internally before moving to compare and contrast so you can be sure that you are not missing anything. So, this is a start towards doing exactly that. If anyone finds an error in my data, please let me know and I accept responsibility for that. I will note the errata and I will fix. However, I do believe that when you start zoning in on a hypothesis straight away, you can miss the bigger picture. Also, I am putting some context back on the table, which has got lost in all the bickering.

If the starting point of your analysis goes something like ‘How much money does C&C take from the community?’ then, straightaway, you are zoning into a specific area without taking a broad picture. In efficient data science, we need to take our biases off the table in order to get a true picture of the data we are looking at. I want to provide a value-free analysis of the financial statements and I hope to make a start here. In this blog post, I am going to try to help you and me to understand, using PASS as an example.

Before I start, I also want to add in a few points about some of the criticisms I am seeing online, as well as some extra contextual information.

‘PASS need to diversify their Portfolio’

From 2014 onwards, I tried to do exactly that. I went through four years of personal hell as a PASS Board member, taking shit from people who just did not believe that business analysis, business analytics or similar related technologies such as Power BI had any place at the PASS table. I spent one whole PASS Summit dealing with people who demanded my time to tell me what they thought of me and my vision – and it was not good – did I really travel thousands of miles to be griped at? Yes, I did, because I tried to help people understand that we needed to diversify to help secure PASS’s financial future and I wanted to build a longer table for community health as well as financial security for a sustainable organisation.

I was trying to ‘diversify’ the Portfolio years ago but SQLFamily, mainly, did not support me. The PASS team supported my vision and they were amazing, and they absorbed a lot of the ‘change management’ part of trying to encourage an established audience to adopt a new audience. I had hoped that the SQLFamily at the time might see into the future and help bring younger and more diverse people with diverse backgrounds into our existing SQLFamily. Instead, it seems that Power Platform was born instead. I do see some overlap but I also see missed opportunities for PASS to be a bigger part of that community story. FWIW I admire the Dynamics Power Platform community for building such a great, sustainable, and fun community and scaling it horizontally and vertically is such a short space of time. I tried to give people that vision but that didn’t happen, and there was a real pushback on me from people who didn’t like the change. I tried to ring alarm bells then about my concerns about financial sustainability and community but I am sorry that did not come across at the time.

Now, five years later, it seems as if SQLFamily people are finally starting to understand that PASS needs to diversify their Portfolio. I told people this years ago, and I tried to set up a Conference to prove it. It was the start of trying to diversify but the reality is, people mainly did not get behind it. The PASS BA footfall just didn’t add up. However, I tried. I could see then, years ago, exactly what is dawning on people now: PASS needs to diversify their Portfolio to continue to be relevant, and to keep cash coming in. On a personal note, it was a hard effort to set up a conference in a timezone that is eight hours away from mine, and no mean feat to set up a conference in a different continent. Note: PASS did not have bottomless pockets then or now (more on this later) so it was a huge personal thankless effort.

The vision that I had then, is pretty much what the Power Platform community looks like now. I wish them all the best and that’s what I wanted for PASS. Fun, vibrant, and it does not have people throwing verbal stones all over the place on social media. The Dynamics community is very healthy with a lot of sponsors and their conferences are nice places to be, with a diverse audience, diverse speaker base which includes young people as well as the older generation of speakers, and it is run by a company that does not seem to experience the same venom over social media as PASS and C&C. Nobody is sending shittagrams to Dynamic Communities or writing blog posts questioning their credibility in any way.

What does that say about the #SQLFamily? Have you looked at how SQLFamily must appear outside of our community to other communities? Sponsors want nice audiences and the online stramash just makes it harder to convince sponsors to participate; they do have a choice of events to support as well. I don’t see Power Platform folks tweeting about getting expletive filled emails.

The PASS Anti-Harassment Policy (AHP)

Every time someone comes to a PASS event and complains about an issue covered by the AHP, that is going to involve legal fees straight away. It’s my guess that C&C are going to seek legal advice to get the best advice on what to do. I believe that is the right thing to do. However, they can’t exactly put a line on the balance sheet that says ‘this is the number of calls that were made about a potential AHP violation.’ That damages the privacy of all parties involved. The AHP is one of the good things about PASS and if it disappears tomorrow, what happens? I am absolutely not complaining about this cost at all. However, in a male-dominated environment, this can get forgotten about; it is part of the male privilege that you don’t have to worry about it. If PASS goes, what happens to this? What does that look like in online world, where people will make false claims about you with no evidence or thought that an accusation does NOT equal evidence? See more about my recent experience here.

Governance

From my reading of the balance statement, there are additional items in here which explain further detail, such as ‘Adjustments to reconcile change in net assets to net cash used in operating activities’. Now, ‘transparency’ depends on the lens that you are looking through. From the accounting perspective, these notes are very good because they add additional detail to show the lineage of some of the numbers that we see in the financials. So, from the accounting perspective, it is very transparent. From the perspective of a DBA with no financial background, this may appear opaque. From the accountant lens, they are probably not sure why they are being accused of being opaque because, from their standpoint and through the accounting lens, this is additional detail which helps guard against potential fraud.

Transparency means different things to different people, you see.

I was on the Board for four years, and then I rolled off the Board. It was a long time for someone to give up so much time, effort and even love into the community. Afterwards, I was pretty burned out and my current understanding is based on my time then, not what I see now. PASS have not contacted me much since, and they have had no input into the current post.

Note that the financials are set up for a not-for-profit and my experience comes from Limited Companies (UK). I also do not have familiarity with the tax situation around not-for-profits and, let’s face it, the tax in the US is a mystery to me. So I have deliberately left it out of my analysis. I have just applied the parts that I feel that I can, and hopefully someone with more time and expertise in not-for-profit accountancy can go through it in more details.

So what do the Financials say?

It can be hard to interpret the financial statements of a not-for-profit; it does not look like a limited company set of accounts. That said, I have tried to add in a few items to note here:

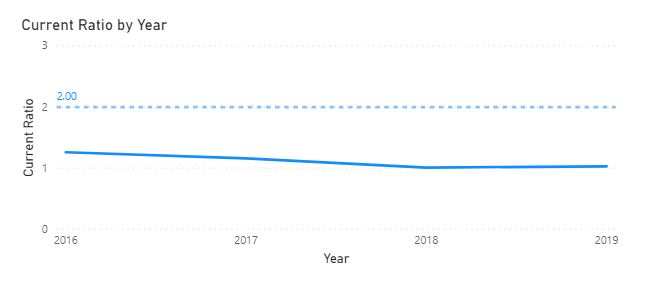

The Current Ratio is the current assets divided by the current liabilities. So, you are checking if the company can cover its short-term liabilities with its short-term assets. Here is the Current Ratio for the past four years for PASS:

| Year | 2019 | 2018 | 2017 | 2016 |

| Quick Ratio ((Current Assets) / Current Liabilities ) | 1.03 | 1.01 | 1.16 | 1.29 |

The table shows that the Current Ratio has fallen in the past four years, and now, the Current Ratio is a tiny smidgen over 1. You can see this value here for the last four years. I have visualized the data below so you can see it below.

What does this current ratio mean for any organization? It means that the organization has to find ways to cut its costs and increase cash flow. From what I can see on the balance sheet, they have been trying to do just that.

What does the Current Ratio mean? In a healthy company, I would see this much closer to 2. The fact that the PASS financials are so close to 1 is a concern for me because it could be better. If the liabilities to up or the financial asset amounts go down, then the Current Ratio would start to dive under 1. It is not the only metric and there are others, but this is a quick and dirty way of looking at liquidity. I have also noted in the guidance notes that PASS have a line of credit agreed which has stayed static for the past few years ($250K, 10% of the total liquidity assets of $2.5 million). I will be interested in finding out the updated credit line in the next set of accounts to see if there has been any changes to the credit availability. So far, so good, but a point of concern for me.

Further review drew my attention to the decrease in the Working Capital over the past four years. I have tabulated the information below. I double-triple-checked my numbers:

| 2019 | 2018 | 2017 | 2016 | 2015 | |

| Working Capital | 97,264 | 31,770 | 402,527 | 830,964 | 1,076,694 |

This means that the Working Capital has shrunk from $1,076,694 to $97,264 within five years. Let me draw that out for you.

In other words, the Working Capital has shrunk to less than ten percent of the Working Capital that was in place five years ago. This metric was actually one of the metrics that meant I did not want to put myself forward for re-election again; I had tried to grow the community to make it more sustainable, and this number made me realize that my efforts were not being accepted by the community. People just didn’t want PASS Business Analytics even though I was sure it would help prevent figures like the aforementioned table. We needed to diversify and it was time for me to hand over the reins to someone else who might find ways that the SQLFamily were willing to accept.

What about Microsoft and PASS?

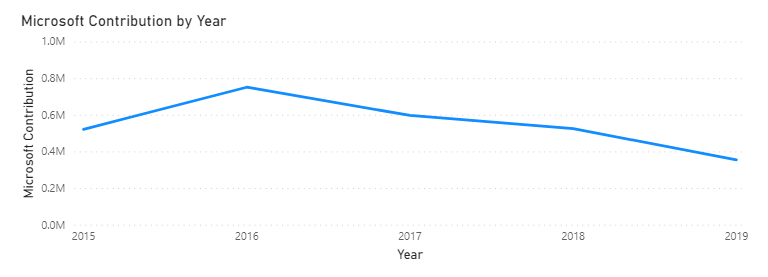

I am just going to copy and paste the comment from the Financial Statements which is repeated throughout all of the years:

Note 8 – CONCENTRATIONS

PASS has a significant volume of transactions with Microsoft Corporation (“Microsoft”) including community support, event sponsorships, conference attendance by Microsoft personnel and expense reimbursements. Approximated revenues generated from Microsoft were $XX000 and $XXX000 for the years ended June 30, XXXX and XXXX respectively.

Let’s take a look at the Microsoft and PASS connection more closely. Let’s see that data for the past few years.

Now, there is a spike around 2016 and I am not surprised by that; PASS had been trying to work with Microsoft on our vision of what the Business Analyst audience might look like for the PASS Business Analytics community, so my guess is that Microsoft offered additional support because we were in their flight path.

PASS have sponsors who are in co-opetition with each other, but fortunately, it seems to work because people play nice. Microsoft are still contributing to PASS, but PASS will need to find other sponsors who may be competitors with one another. Note also that in 2017, according to the Financials, ‘Charter and Founder Member Support’ ended which had contributed $96K that year.

What can PASS and the community do?

PASS need to execute their virtual event, and do it well. To do that, PASS need to grow their existing audience, sell sponsorships and tickets, and then regroup to understand better what the audience needs. PASS / C&C have skin in the game and that’s shown by them absorbing some of this cost.

In my envisioning as part of the Special Projects portfolio, I recommended that PASS get involved in other topics such as BA Days, Excel Days, Artificial Intelligence ‘Days’, like SQLSaturdays. Given that we had been disappointed by the failure to adopt PASS Business Analytics, I can understand the reticence to try anything new.

Sponsors may well baulk at supporting PASS, given the high temperature on social media at the moment. For me, the minutes of the meetings are all there, and so are the Financial statements. It should not be a surprise that PASS can’t afford to dish out free passes all over the place, and that’s clear from the statements that they publish regularly. It’s important to try and read the minutes and follow the Financials.

I do wish PASS all the best. We are all data professionals, and if you want to work on helping to secure PASS, do the following:

- Give them as much social media love as you can. Emulate Power Platform if you need inspiration.

- Buy a ticket for the Conference or encourage others to do so. We are all highly paid professionals.

- Be nice to the Sponsors. RT them, like them, whatever. They also have skin in the game and they are invested.

- Be nice to the first timers who are trying to get involved in the community. I bet people are running for cover right now. Please, think about how our community comes across.

And please don’t beat up the Board. If you take one thing away from this post, note that they are a really hard job to do. Please support them if you can. They are facing a grinding financial situation on top of work (they are volunteers) and in the face of the coronavirus. I’ve had people in my family die of the virus. Please be kinder to one another. The PASS Board have a thankless job on their hands and I bet a few sleepless nights, too. Instead of writing things to hurt people, why not step up to the plate to do something about it like they (and I) did?

About the revenue diversification: you can sell a new product to existing customers, an existing product to new customers, or a new product to new customers. The latter is the most expensive one by a long shot because you have to both build the new product, AND pay for it.

The BA Conference was a new product to new customers, and I think that’s why a lot of us had trouble getting behind it.

I know very little about PASS outside of what I read above, but from the article it sounds that Microsoft is one (big) customer, and was an existing one.

That’s part of the problem: seeing the advertisers as the customers.

PASS catered to their advertisers, and like many ad-focused media companies, they’re seeing the effects of investing in ads rather than content. Never forget who your real customers are: without satisfying the end users, they simply won’t pay for your product. There’s a market for selling spam, but it’s not sustainable long term.

Very good blog post, Jen. And also a very sad one at the same time, on more than one level too.

I’d like to discuss further as I write my own blog post on this topic. Reach out when you have a moment to spare and we’ll catch-up. Cheers!

Keep fighting the good fight. Best regards,

-Kev